CAGR Insights is a weekly newsletter full of insights from around the world of the web.

What we’re reading this week

- 10 changes in draft Income-tax Rules 2026 : Read here

- Will capex finally help drive India’s economic growth? Read here

- Why Consensus Fails: Read here

Impact of the India-EU FTA Deal on Key Export Sectors

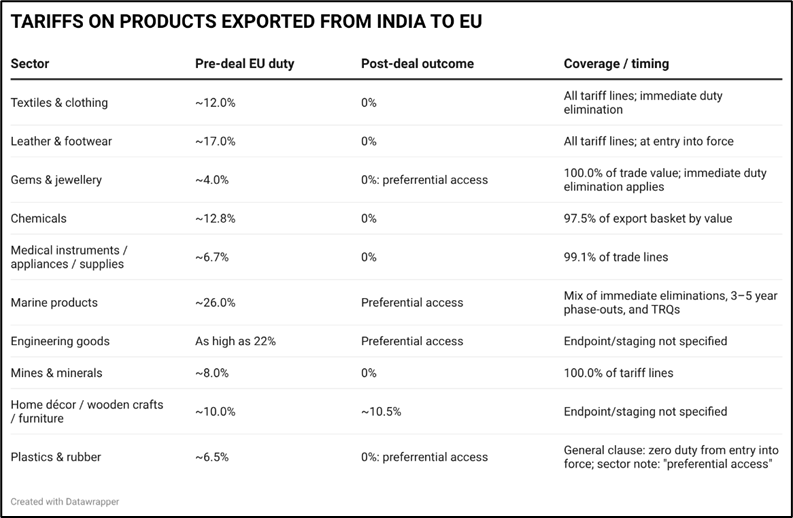

On 27 January 2026, at the 16th India–EU Summit, India and the European Union (EU) concluded a historic, comprehensive Free Trade Agreement (FTA). This agreement is intended to deepen and stabilize trade between the two major markets. It will also be linking India, the world’s fourth-largest economy, with the EU, the world’s second-largest economic bloc.

What is a free trade agreement?

- In contrast to what the name might suggest, what gets agreed upon in a free trade agreement (FTA) is not all that “free” and is not solely about trade.

- An FTA is a comprehensive form of collaboration with legally binding agreements in many domains. It establishes new ground rules on, for example, product requirements, import tariffs and taxes, and company rights such as intellectual property and protection.

This deal will be pivotal in the history of both economies. In this article we will focus on the key gains for the Indian economy.

Immediate duty elimination lifts competitiveness for India’s labor-intensive sectors. Further, staged reductions and tariff-rate quotas create additional pathways in more sensitive product lines. This will help firms plan capacity, contracts, and investment with greater certainty.

For Indian producers, the upside is not just higher volumes but also a push toward upgrading. This is because sustained EU market access typically requires tighter standards, traceability (source of origin), and process discipline. While some of these conditions have been relaxed in the FTA, they are not eliminated. This means that firms will have to adapt to move up the value chain. Those that cannot, may remain stuck in low-margin segments.

The question now is what lies ahead for India and how it can translate improved market access into sustained gains across these key sectors. The opportunity is significant, but real outcomes will depend on how effectively Indian firms and policymakers address competitiveness, compliance, and scale.

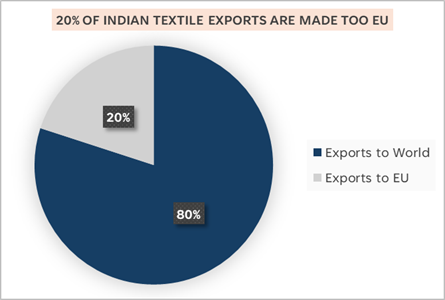

Textiles

- For an industry that employs over 45 million workers across spinning, weaving, knitting and garmenting, and that has labored under uneven trade terms for years, the moment felt historic.

- In fiscal 2024-25, India’s textile and apparel exports totaled about $37 billion (India is amongst the top 5 global exporters of textile and clothing). Out of this ~20% of the exports are currently made to EU. The tariff reduction is important because it restores parity with competitors such as

- Bangladesh, which benefits from zero duty under the EU’s Everything but Arms scheme. But Bangladesh is set to lose this zero-duty access from November 2026. This change will give India a major competitive advantage in textiles.

- Vietnam and Turkey, which enjoy preferential access through their regional trade arrangements. However, rising wages in Vietnam and currency volatility in Turkey have increasingly pushed global brands to diversify their sourcing.

- Larger firms such as Arvind, Shahi Exports, KPR Mills and Welspun have already invested heavily in automation, sustainability and traceability systems to align with rising European standards.

- Smaller manufacturers are adopting wastewater recycling, cleaner energy systems and digital compliance platforms that meet strict EU due diligence rules.

- Textile industry groups are now seeking supportive measures from the Centre to help smaller exporters meet compliance costs. These include credit lines tied to green upgrades, streamlined imports of advanced machinery and logistics enhancements that can cut freight costs and delivery times.

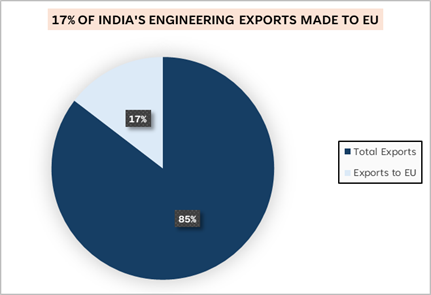

Engineering Goods

- The EU currently absorbs ~17% of India’s engineering exports, translating to roughly $20 billion annually.

- Key export categories include iron and steel ($6-7 billion), industrial machinery ($5 billion), and auto components ($3 billion).

- With shipments to the EU reaching nearly $11 billion in November 2025, exporters expect the FTA to further accelerate momentum.

- This deal is also going to make MSME’S gain significantly. 60% of EEPC India’s members are MSMEs, largely involved in the exports of iron and steel products as well as electrical machinery.

- However, the benefit of this agreement will be subject how companies are able to resolve challenges posed by CBAM.

- CBAM is a climate-linked trade policy designed to prevent “carbon leakage” by imposing a carbon cost on imports of emission-intensive products.

- For Indian engineering exporters, especially in carbon-intensive segments such as iron, steel, and aluminum, CBAM could increase compliance costs unless firms are able to demonstrate lower emissions intensity or align with EU carbon pricing norms.

- Exporters have flagged challenges around access to verified emissions data, certification costs and the absence of mutual recognition frameworks.

- The iron and steel industry accounts for 90% of India’s CBAM exports to the EU and is, therefore, particularly exposed. Although these exports accounts for only 0.2% of the country’s GDP, the CBAM would have a significant impact on Indian exports.

- The effects of CBAM on the Indian steel industry are likely to be uneven and unfair, with the larger players adapting more quickly and relatively more easily than the smaller players.

- On the positive side, Indian exporters can shift to more environmentally friendly production methods to mitigate the impact of the tax. This could result in increased investment in decarbonization technologies and processes in the sectors concerned.

- Initiatives taken by Indian Companies to meet the standards of CBAM

- JSW Steel is strengthening systems to track and report product‑level carbon emissions, enabling accurate carbon footprint measurement required for EU imports.

- L&T reports total emissions of about 8.1 billion kg CO₂e in 2025 across Scope 1 (direct), Scope 2 (energy), and Scope 3 (supply‑chain) emissions. A majority (~97%) of emissions come from Scope 3, especially from purchased goods and services — showing they’re tracking value‑chain emissions, which is essential for comprehensive carbon disclosures that are relevant under mechanisms like CBAM. It secured a US $700 m sustainability‑linked trade facility linked to greenhouse gas emission intensity and water‑use metrics embedding climate performance into financing decisions. L&T aims for carbon neutrality by 2040.

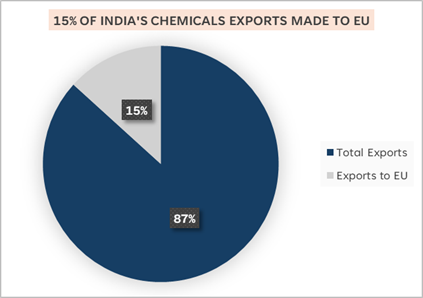

Organic Chemicals

- The FTA is going to strengthen India’s position in becoming a global chemical manufacturing hub.

- But the FTA’s impact won’t obviously be uniform across the chemical landscape. Here’s where the surge is expected to be most noticeable:

- Specialty Chemicals

- Agrochemicals

- Dyes & Pigments

- Pharma Intermediaries and API’s

- Benefits of the “Co-Equal Rule”

- The India-UK FTA introduces a new concept called the co‑equal rule, which is a big win for exporters in sectors like specialty chemicals.

- Traditionally, to get tariff benefits under a trade agreement, a product had to meet specific Rules of Origin, which means a certain percentage of its materials had to come from the exporting country.

- This often made it harder for exporters who sourced ingredients or components from different countries.

- With the co-equal rule, materials from India and the UK will be treated equally when calculating whether a product qualifies as “originating” for duty-free access.

- For example, if an Indian company is making a specialty chemical that uses some inputs from the UK and some from India, with the co-equal rule, both sets of inputs will now count toward meeting the requirement. The final product will still qualify for tariff-free export.

- Strategic Benefits for the Indian Chemical Industry

- Regulatory Support and Faster Market Access – One of the most powerful aspects of the India-UK FTA is the recognition of Indian regulatory systems. By aligning India’s GMP with UK standards, the agreement will shorten product approval timelines and reduce redundant audits. This will not only lower compliance costs for Indian exporters but also make it easier for UK buyers to source from Indian suppliers with confidence.

- Boost to SME Exporters and Tier-II Cities – India’s small and mid-sized chemical firms in hubs like Vapi, Surat, Ankleshwar, and Dahej have powered exports but struggled to enter markets like the UK due to high tariffs and red tape. The new India-UK FTA cuts these barriers, letting SMEs access the UK directly with simpler rules and lower costs. Per IBEF, this could boost SME share in bilateral trade by 20-25% within two years, creating jobs and balanced growth.

Conclusion

- What sets this trade agreement apart is its potential to change how the world sees Indian industries.

- It’s not just about increasing exports or saving on tariffs. It’s about shifting from short-term opportunities to long-term partnerships. With better regulatory alignment and more predictable compliance rules, Indian companies now have a real chance to become trusted suppliers in the global market.

- This shift is also happening at a crucial moment. Many countries are rethinking their dependence on single-source suppliers like China. India is stepping up with strong scientific talent, growing infrastructure, and a clear policy push.

- But this opportunity comes with responsibility. The real impact will depend on how quickly Indian firms adapt, upgrade, and build the kind of trust that lasts.

Sources

- https://www.indiatoday.in/india-today-insight/story/how-indias-trade-pact-with-eu-is-knitting-the-future-of-its-textile-industry-2860015-2026-01-29

- https://www.eepcindia.org/export-statistics:

- https://www.icwa.in/show_content.php?lang=1&level=3&ls_id=14128&lid=8575

- https://chemexcil.in/uploads/files/India%E2%80%93EU_FTA_Indias_Gain_Chemicals_Sector27JAN.docx

- https://www.scimplify.com/blogs/india-uk-fta-opportunities-indian-chemical-industry

****

That’s it from our side. Have a great weekend ahead!

If you have any feedback that you would like to share, simply reply to this email.

The content of this newsletter is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction. The content is distributed for informational purposes only and should not be construed as investment advice or a recommendation to sell or buy any security or other investment or undertake any investment strategy. There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any information outlined in this newsletter unless mentioned explicitly. The writer may have positions in and may, from time to time, make purchases or sales of the securities or other investments discussed or evaluated in this newsletter.