CAGR Insights is a weekly newsletter full of insights from around the world of the web.

What are we reading this week?

- Why are Indian households shifting from fixed deposits to SIP investments? Read here

- The Reign of the Dollar Is Coming to an End. What Investors Can Do About It. Read here

- India is rising in the new world order: Read here

How to Make Your Bank Actually Listen

The script-flipping moment in banking doesn’t happen when you scream at a customer service executive. It happens when you stop being a “customer” and start being a “complainant” under the RBI’s Integrated Ombudsman Scheme.

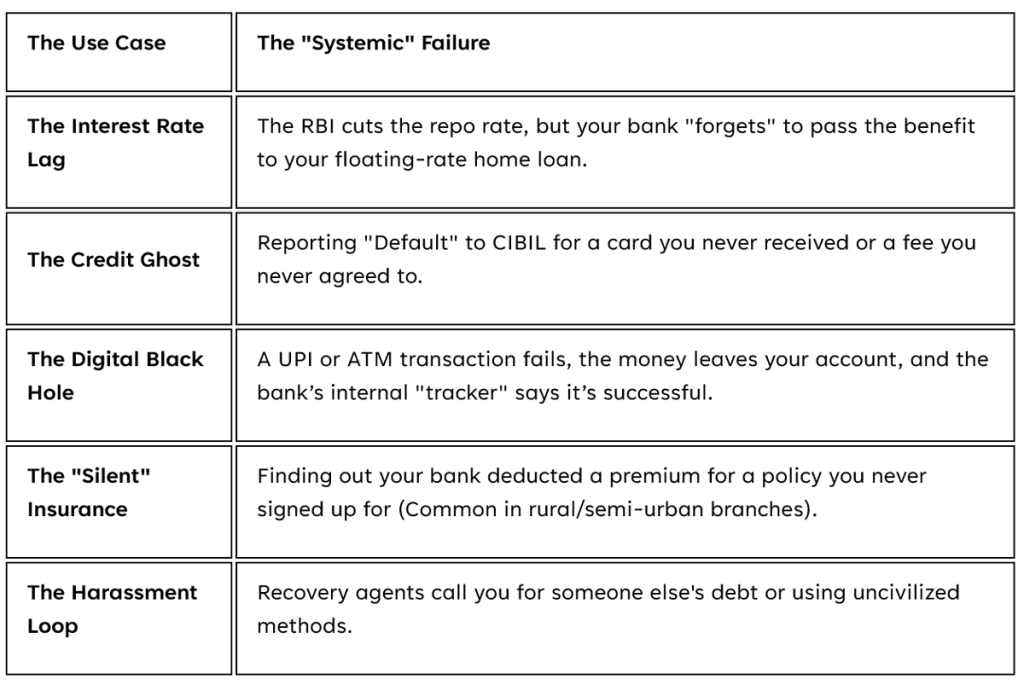

Why Do Banks Ignore You?

Banks are slow to change. Basically, their customer service is set up to slow you down. They use robotic, copy-pasted replies to wear you out until you eventually just give up.

But there is a “trapdoor” in the Indian financial regulation system. When a bank receives a notice from the RBI Ombudsman, the cost of fighting you suddenly becomes higher than the cost of fixing the mistake.

The Playbook: Where the Ombudsman Actually Wins

RBI Ombudsman won’t fix every small, annoying thing that happens. However, for big problems that are clearly the bank’s fault (like a “system” error), it works like a precise tool to cut through the bank’s excuses and fix the specific issue. Here is where you use it:

When the Bank Locks the Door and Calls You a Trespasser

Anirudh was a responsible customer who never missed a single payment. He was incredibly proud of his perfect credit score. But one day, the bank made a mistake that he couldn’t fix just by being a good customer. As his credit card bill due date approached, Anirudh tried to log in to pay. The card was gone. No “Renew” button.

- No “Pay Now” option.

- The banking app acted as if he had never owned a credit card in his life.

The bank had deactivated his old card but failed to deliver the new one. They essentially locked the front door of the bank while he was standing outside with the cash in his hand.

Anirudh didn’t sit back. He sent an urgent email before the due date:

“I cannot see my card. I cannot pay through the app. Please, auto-debit the dues from my savings account immediately so I stay on track.”

The bank’s response? Total silence. No auto-debit happened. No one called him back. He was trapped in a digital void.

Nine days later, the system finally “woke up.” Anirudh paid the full amount the second the button reappeared. He thought the glitch was over, but he was wrong.

Months later, he applied for a home loan. The loan officer frowned at the screen. “Sir, you have a 9-day delinquency on your record. Your CIBIL score has cratered by 50 points.”

Because the bank’s computer saw a late payment, it didn’t care why it was late. To the algorithm, Anirudh was now a “risky borrower.” His home loan interest rate was hiked, potentially costing him lakhs of rupees over the next two decades.

When Anirudh complained, the bank’s customer service gave him the ultimate insult: “The payment was late. The system is automated. We cannot change it.”

Anirudh stopped trying to be “nice” and started playing by the bank’s own legal rules.

He didn’t send an angry rant. He sent a Timeline of Failure.

- Evidence A: The date his card was deactivated without notice.

- Evidence B: The email he sent before the due date asking for an auto-debit.

- Evidence C: The proof that the bank failed to deliver the renewal card.

Under the cold light of a regulatory inquiry, the bank’s “automated system” excuse collapsed. They admitted:

- The card had expired.

- The renewal was never delivered.

- The customer was physically prevented from paying.

The bank was forced to contact CIBIL and suppress the DPD (Days Past Due) entry. Anirudh’s score was restored to its rightful place.

But this victory didn’t happen overnight, it required navigating a specific legal hierarchy that every banking customer must follow.

You cannot jump straight to the RBI. The Ombudsman is the Level 3 boss; you must clear Level 1 and 2 first.

Step 1: The Paper Trail (Day 1)

Skip the phone calls. Send an email to the bank’s Grievance Redressal Officer (GRO). This starts the 30-day “cooling-off” period.

Email the bank and list exactly when each problem happened. Show that you tried to fix it, but their customer service failed to help. Include proof (like screenshots or emails) for everything.

Step 2: The Wait (Day 31)

If the bank:

- Rejects your complaint.

- Offers an unsatisfactory “middle ground.”

- Simply doesn’t reply for 30 days. You are now eligible.

Step 3: The CMS Portal (The Final Move)

Go to the RBI Complaint Management System (CMS) website. This is where the narrative shifts. You aren’t arguing with a bot anymore; you are filing a case that goes into the bank’s “Regulatory Non-Compliance” statistics.

The Moral of the Story

In the digital age, a bank’s “glitch” is often treated as the customer’s “fault.” If a bank blocks your ability to pay, don’t just wait for them to fix your attempt to pay immediately. That paper trail is the only thing that will save your credit score when the system turns against you.

****

That’s it from our side. Have a great weekend ahead!

If you have any feedback that you would like to share, simply reply to this email.

The content of this newsletter is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction. The content is distributed for informational purposes only and should not be construed as investment advice or a recommendation to sell or buy any security or other investment or undertake any investment strategy. There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any information outlined in this newsletter unless mentioned explicitly. The writer may have positions in and may, from time to time, make purchases or sales of the securities or other investments discussed or evaluated in this newsletter.